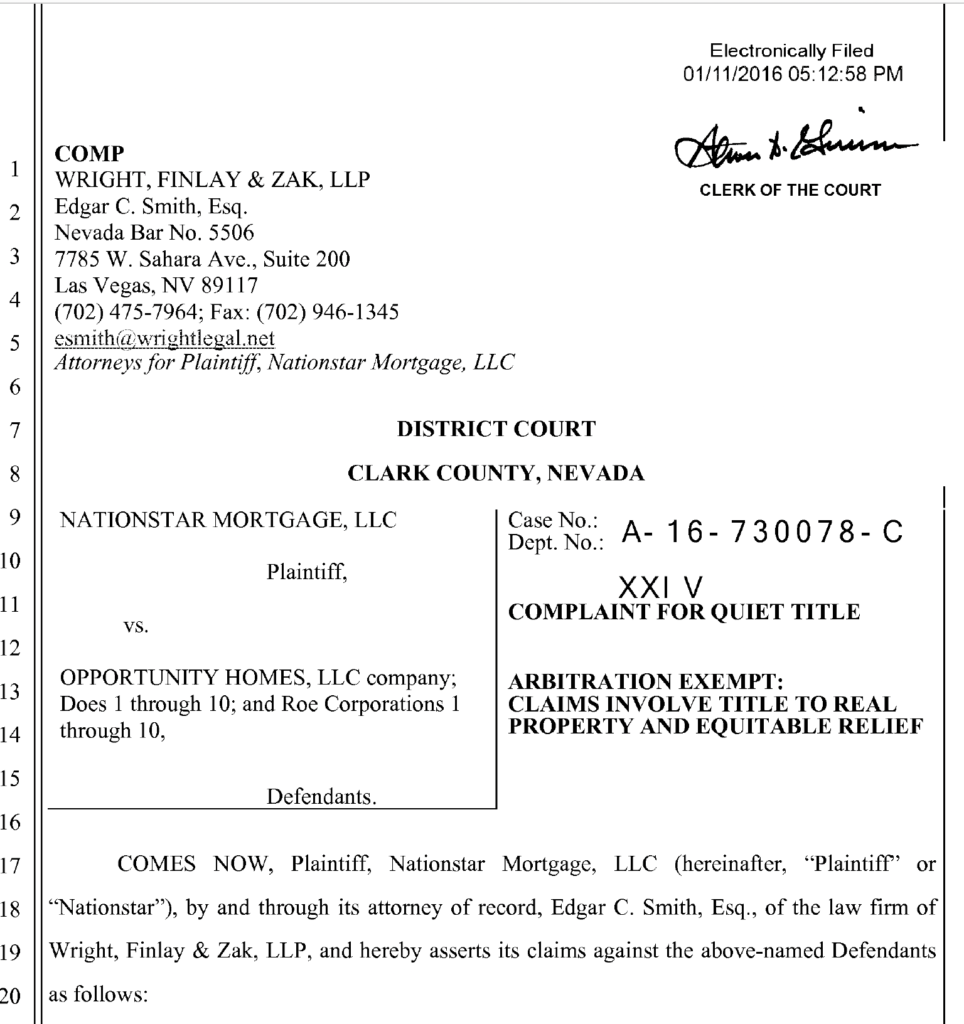

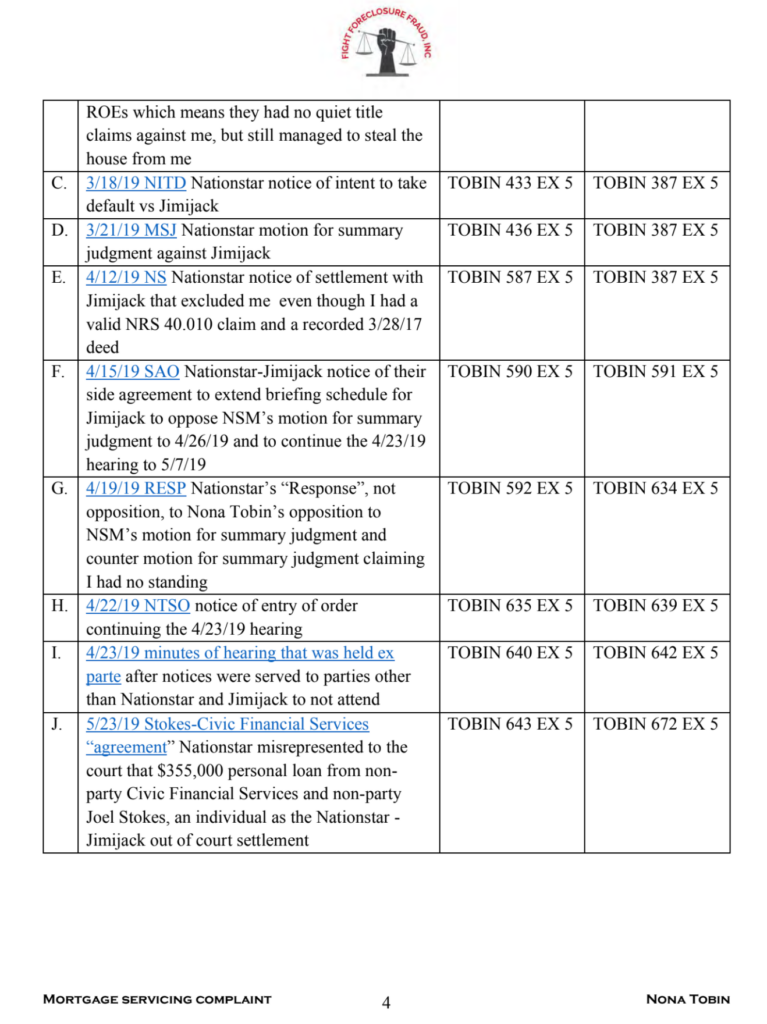

1/11/16 Nationstar started by filing to quiet title vs. the wrong buyer.

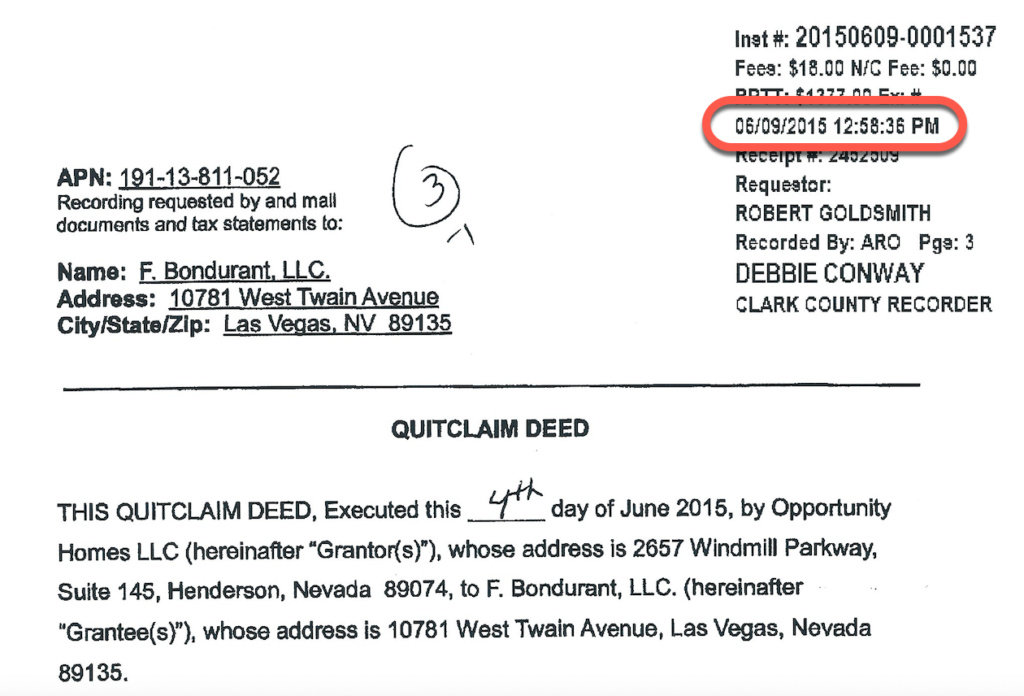

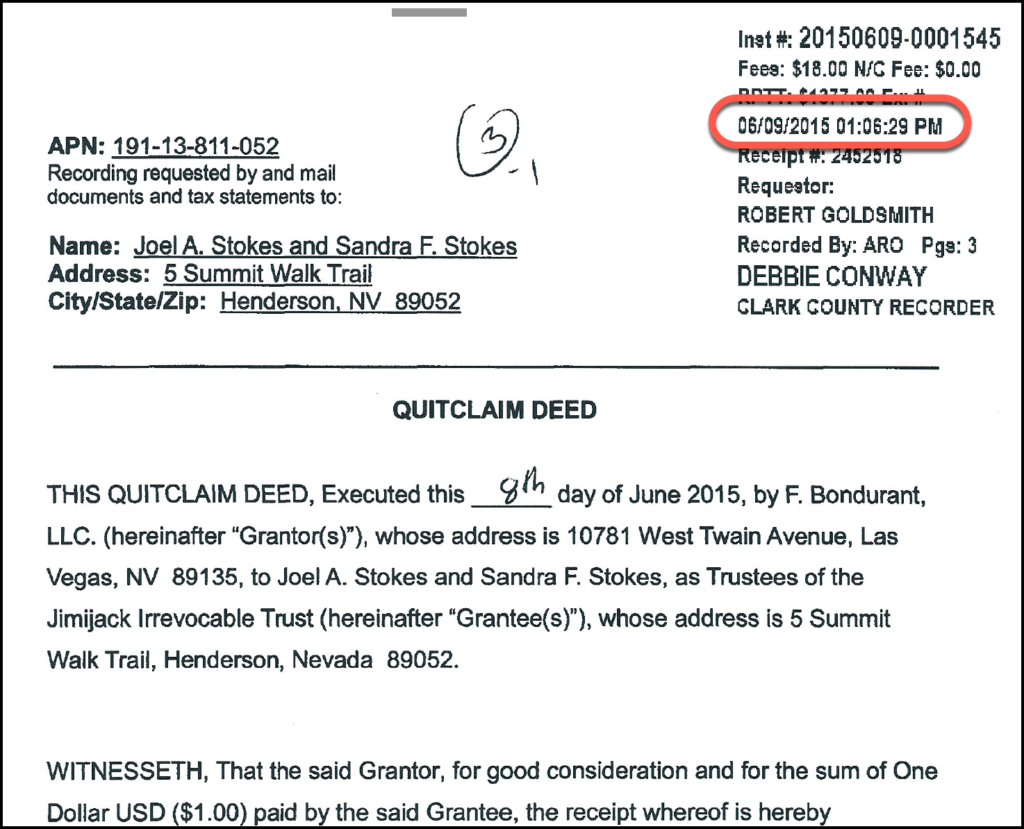

Opportunity Homes LLC was disinterested. Two others had recorded deeds on 6/9/15

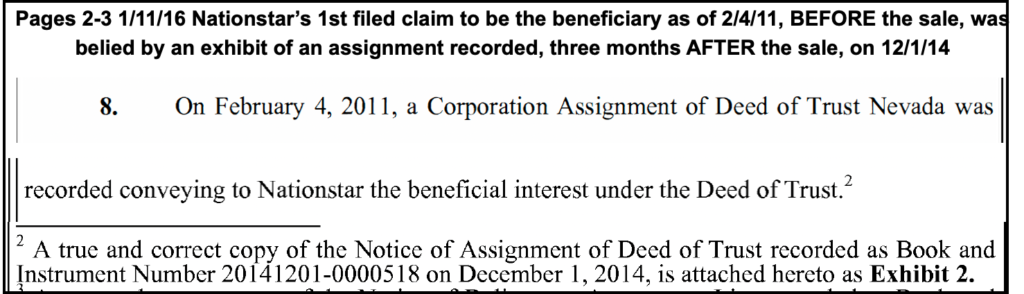

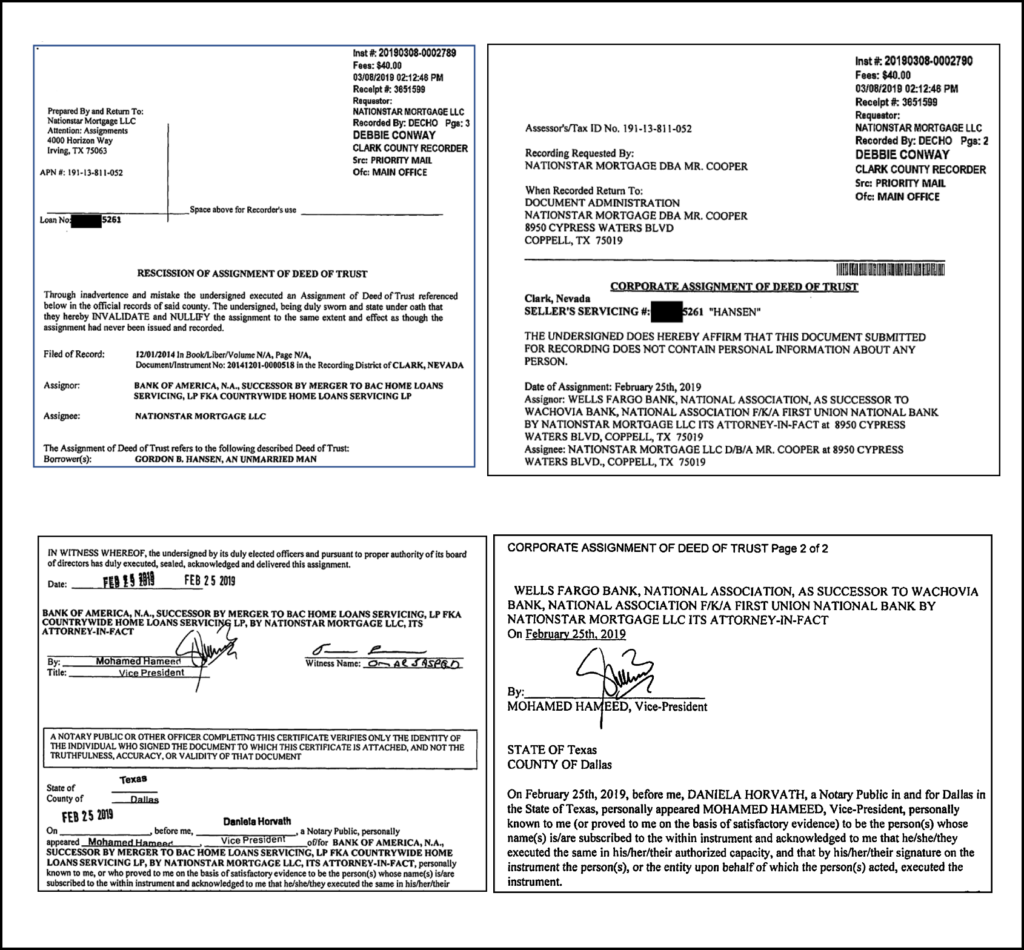

1/11/16 Nationstar also lied about how it became the beneficiary of the 1st deed of trust that was extinguished by the 8/15/14 HOA foreclosure sale.

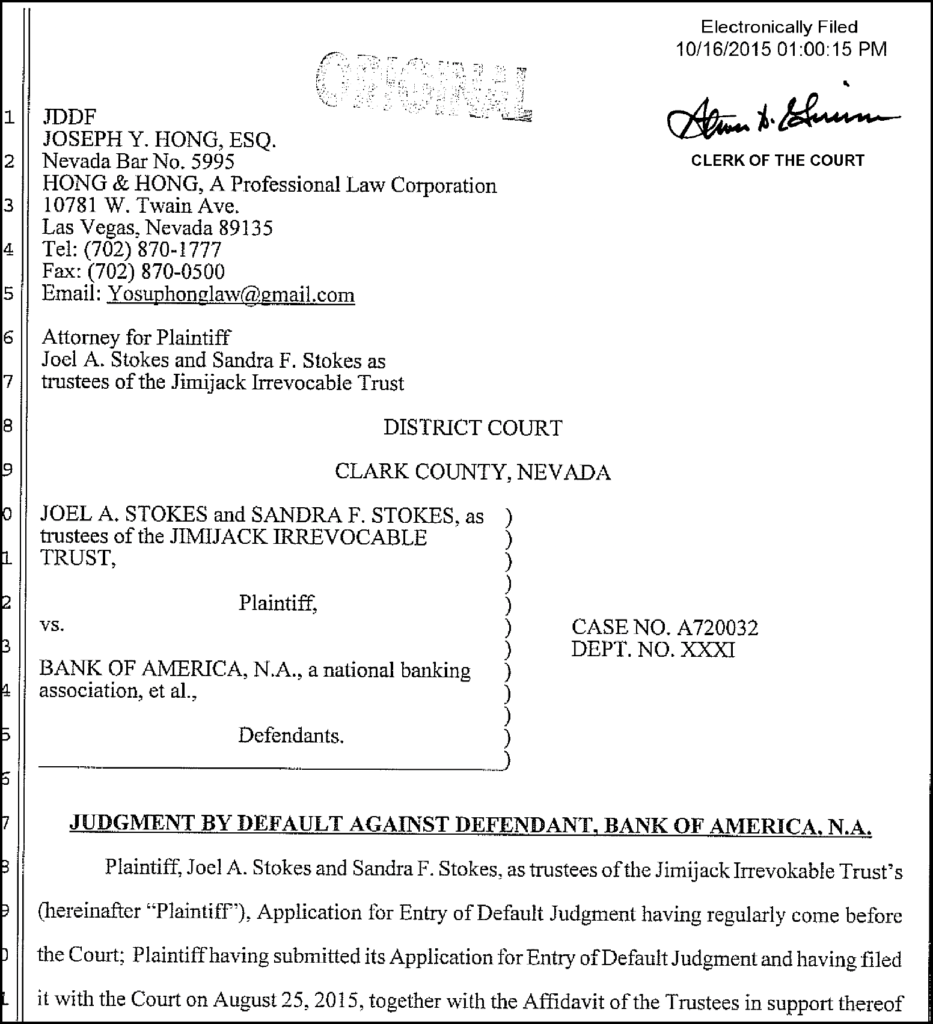

Jimijack somehow already had a default judgment by suing disinterested Bank of America.

How could that happen?

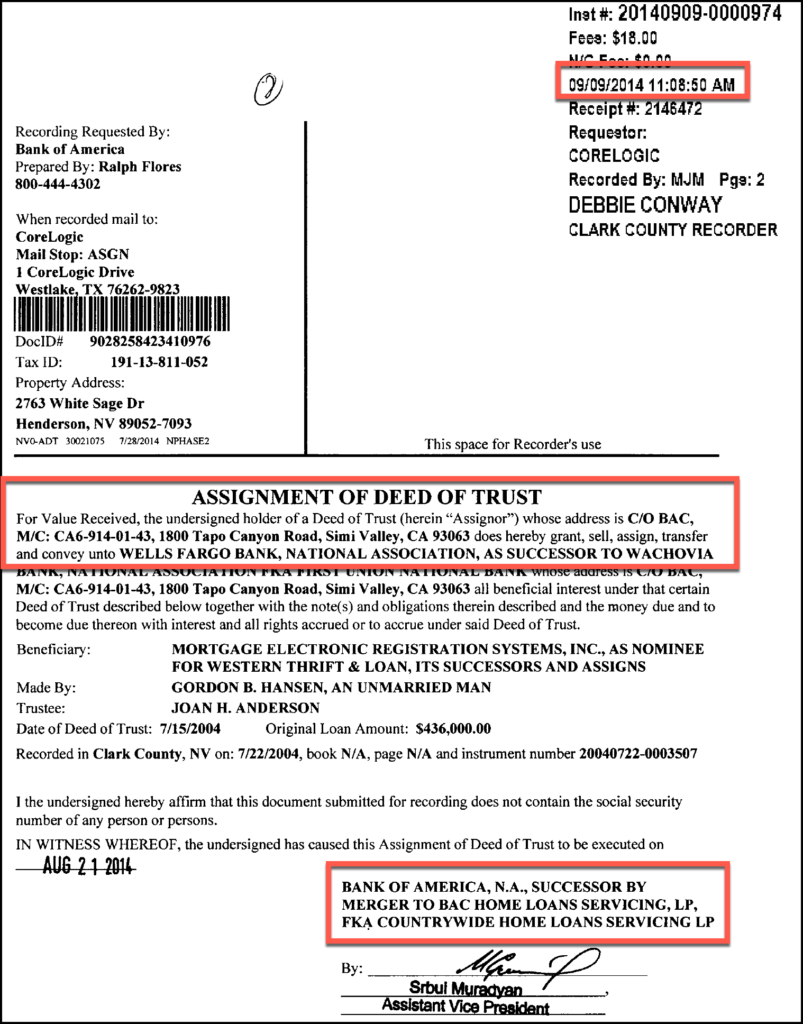

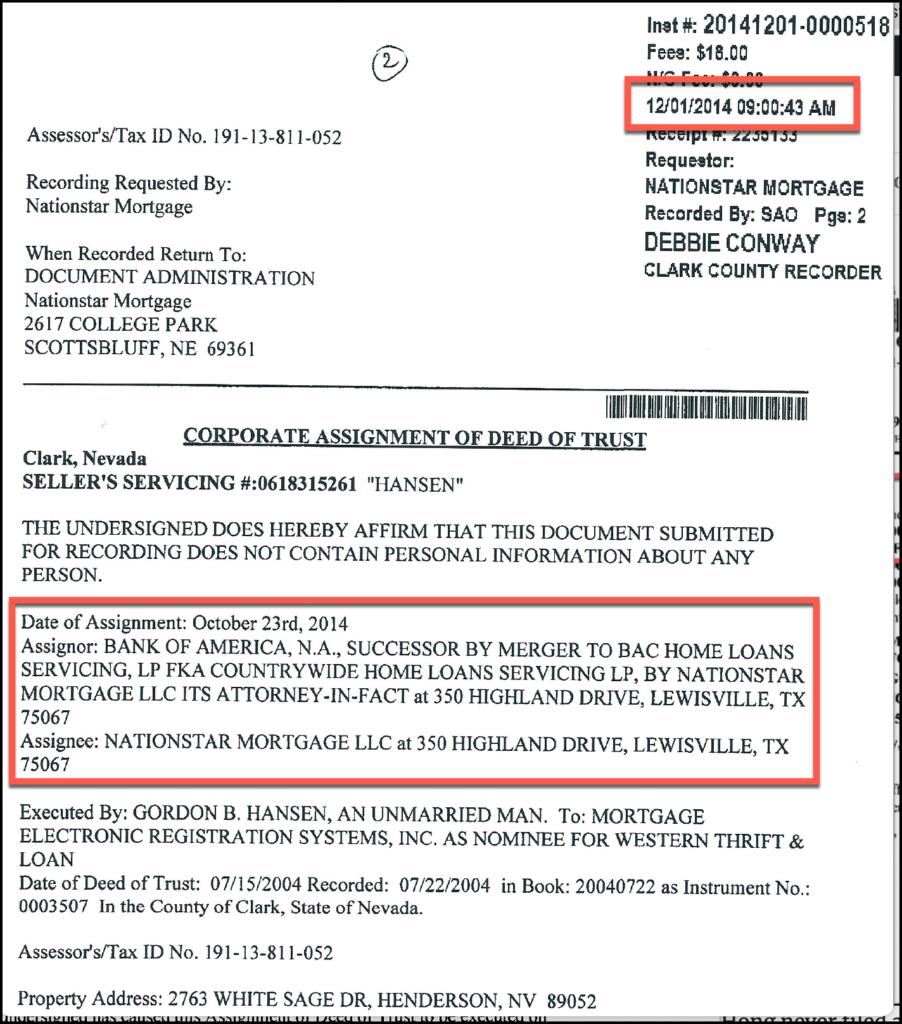

There were TWO banks with recorded claims that BANA gave its beneficial interest to it:

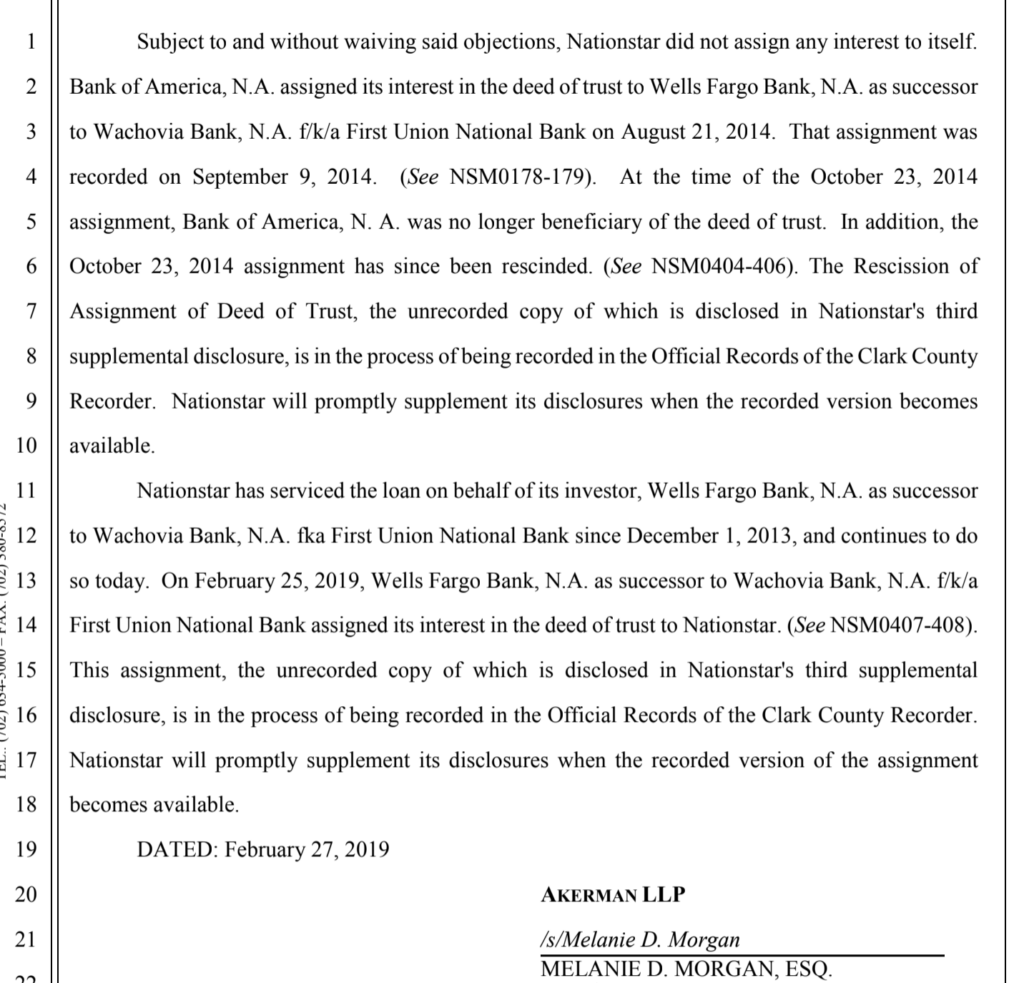

9/9/14 BANA recorded it assigned its interest, if any, to Wells Fargo on 8/21/14

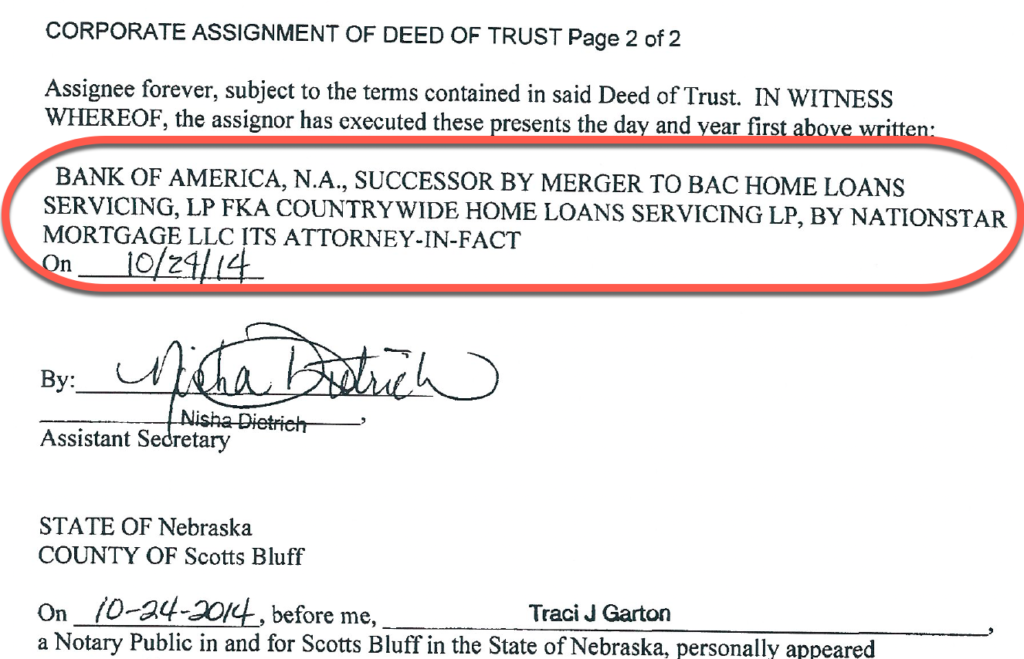

12/1/14 Nationstar recorded it had BANA’s unrecorded power of attorney to assign BANA’s interest, if any, to itself on 10/23/14

Nationstar didn’t file any claims against me as the trustee of the Gordon B. Hansen Trust or as an individual .

Nationstar got summary judgment by claiming BANA gifted the $389,000 loan balance to it 3 months after BANA gifted it to Wells Fargo immediately after it was extinguished by the HOA foreclosure.

How did that happen?

Neither Jimijack nor Nationstar nor the HOA have any filed claims but all got summary judgment by getting my claims precluded and my evidence stricken and their fraud undetected

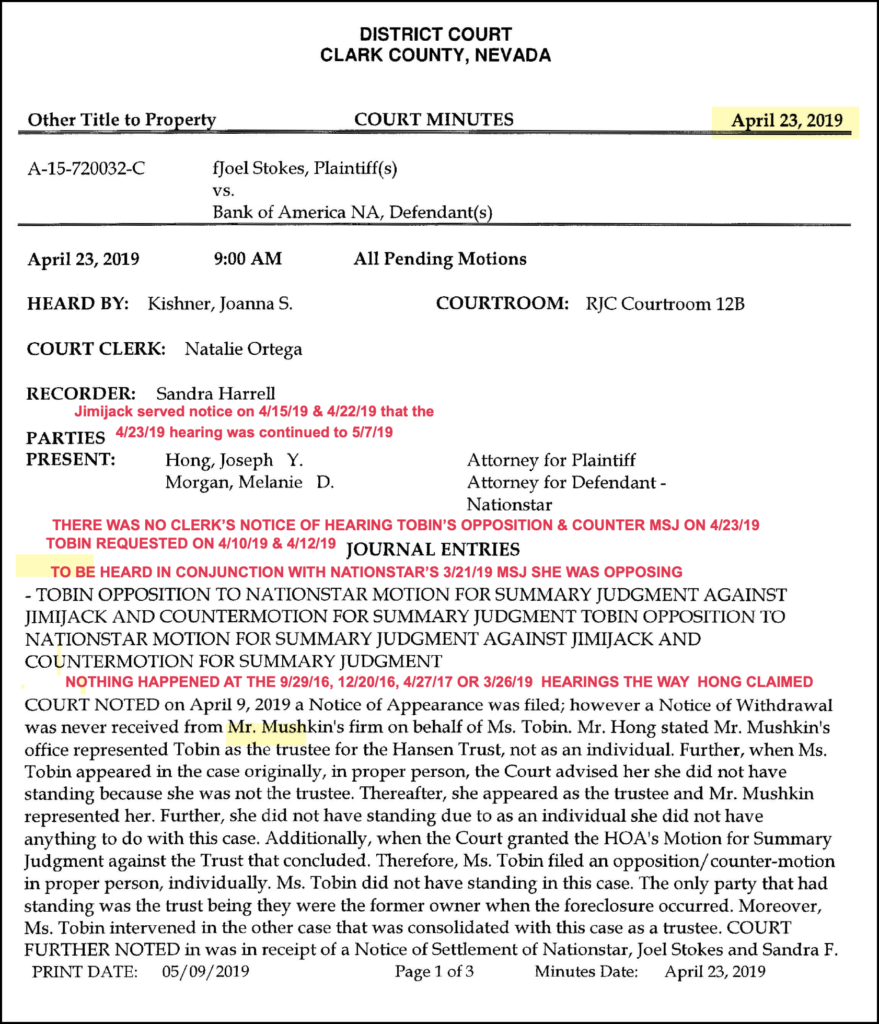

Nationstar quietly dismissed all its filed claims without adjudication on 2/20/19, 3/12/19, 4/23/19, and 5/31/19

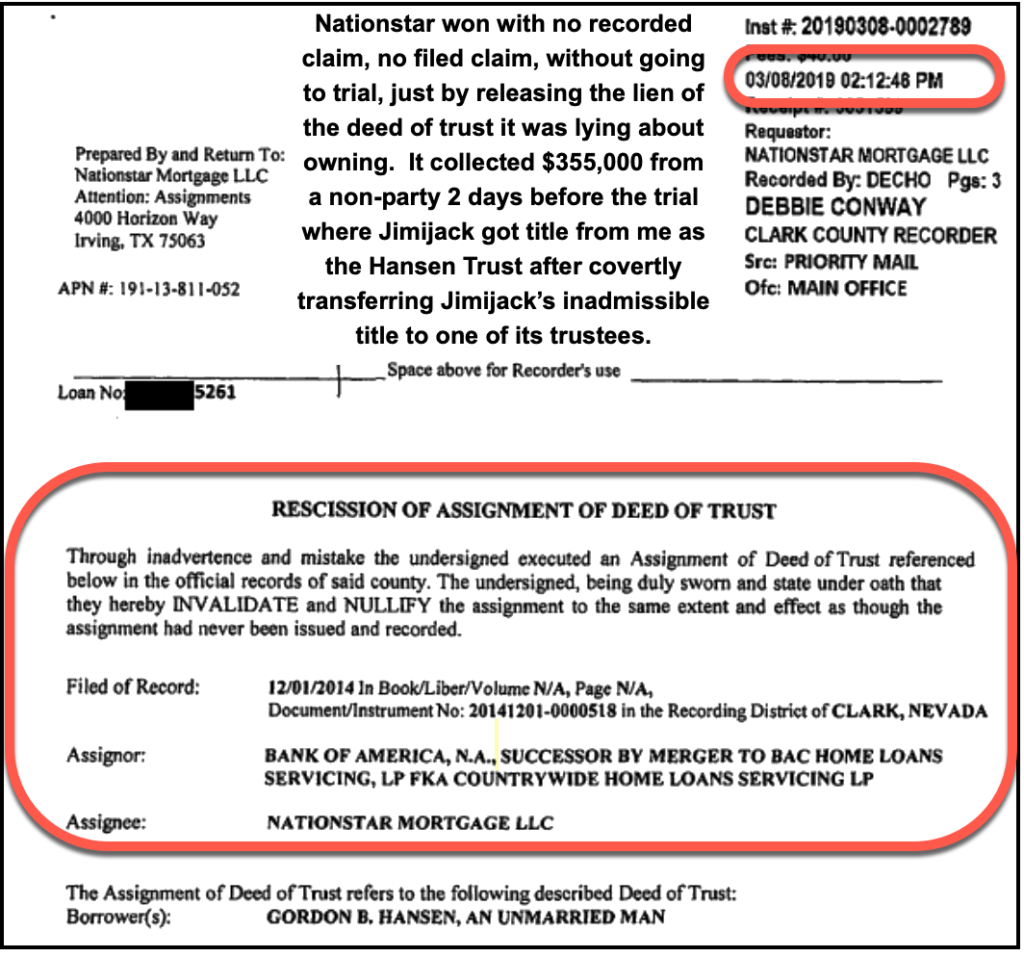

Nationstar covertly recorded a rescission of its claim to be BANA’s successor in interest

Nationstar’s attorney and Jimijack’s attorney told the judge to ignore all my evidence because I wasn’t really a party

Hong concealed from the court Jimijack covertly dumped its inadmissible deed

Joel Stokes encumbered the property with $355,000 CVS loan to launder Nationstar’s pay off for releasing the lien of the 1st DOT

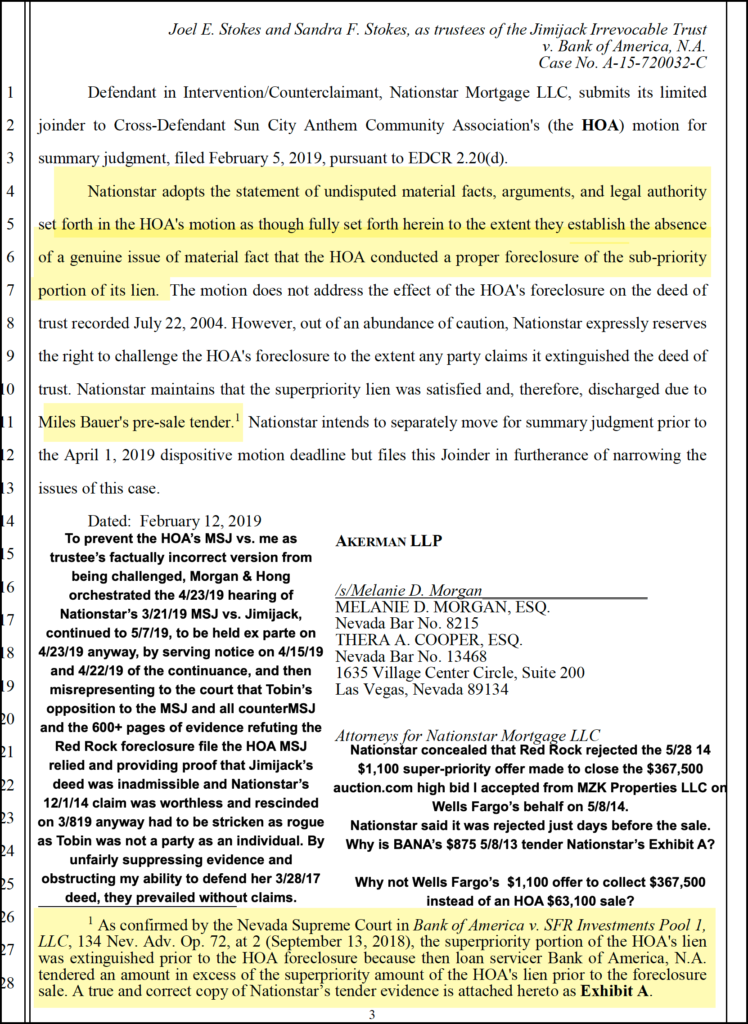

Nationstar’s attorneys knew that Nationstar rescinded its claim that got its 2/12/19 joinder granted and knew its 3/8/19 claim recorded after discovery ended was fraudulently executed by a robosigner

Nationstar’s attorneys knew the PUD Rider prohibited turning the rejection of assessments into a de facto foreclosure and that’s what they were doing by this trick

Akerman still went all in two days before the trial with the quid pro quo

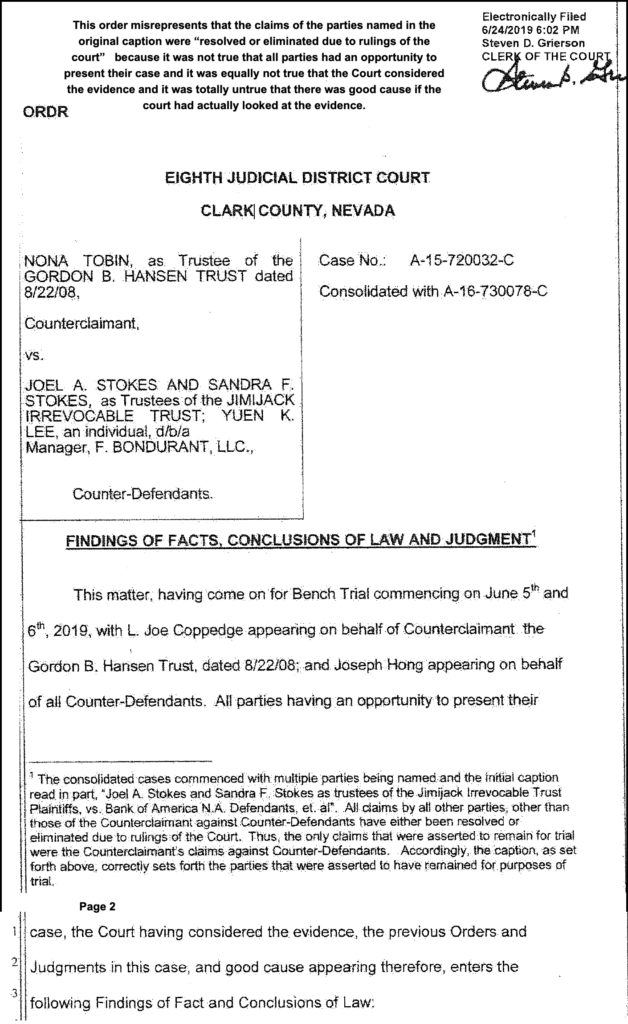

None of the elements for quiet title were met at the 6/5/19 trial as no party was at the trial who had any interest in the title to protect, and all documentary evidence was unfairly excluded.

The necessary elements of a declaratory relief or quiet title claim are as follows:

(1) there must exist a justiciable controversy; that is to say, a controversy in which a claim of right is asserted against one who has an interest in contesting it;

(2) the controversy must be between persons whose interests are adverse;

(3) the party seeking declaratory relief must have a legal interest in the controversy, that is to say, a legally protectable interest; and

(4) the issue involved in the controversy must be ripe for judicial determination.

Kress v. Corey, 189 P.2d 352, 364 (Nev. 1948)

The elements for a claim of quiet title were NOT met in the 1st action.

No claims were properly adjudicated based on judicial scrutiny of verified evidence supporting claims by parties with STANDING.

1. Action may be brought by any person against another who claims an estate or interest in real property, adverse to him, for the purpose of determining such adverse claims. NRS 40.010;2. Complaint must be verified. NRS 40.090-1;

3. Summons must be issued within one year of filing the complaint and served per NRCP. NRS 40.100-1;

4. Lis Pendens must be filed with the county recorder within 10 days of filing of the complaint. NRS 40.090-3;

5. Copy of the Summons must be posted on the property within 30 days after the summons is issued, and an affidavit of posting must be filed with the court. NRS 40.100-2;

When a borrower signs a promissory note, he is agreeing to pay the lender a specific amount of money according to certain conditions. In order for the lender to protect his interests, he will require that the borrower sign a mortgage or similar security instrument in favor of the lender. This may be in the form of a mortgage or a deed of trust. Whichever document is used, the purpose of both types of documents is to secure the note and offer protection to the lender.

Depending on where the property is located, state law will determine which type of security instrument must be used. In title theory states, a mortgage is used and it conveys ownership to the lender. A clause in the mortgage provides that title reverts back to the borrower when the loan is paid. In lien theory states, the mortgage creates a lien only on the property and the title remains with the borrower. The lien is removed when all the payments have been made.

Some states are considered modified lien theory states and in these states the title remains with the borrower, but the lender may take title to the property if the borrower defaults.

The basic difference between the mortgage as a security instrument and a Deed of Trust is that in a Deed of Trust there are three parties involved, the borrower, the lender, and a trustee, whereas in a mortgage document there are only two parties involved, the borrower and the lender. In a Deed of Trust, the borrower conveys title to a trustee who will hold title to the property for the benefit of the lender. The title remains in trust until the loan is paid.

Often a title company, escrow company or bank, is listed as the trustee on the Deed of Trust. When the loan has been paid, the trustee will issue a release deed or trustee’s reconveyance deed. This deed of reconveyance should be recorded at the county recorder’s office, to make public notice that the loan has been paid and that the lender’s interest in the property has ended.

Another difference between a mortgage and a deed of trust is the manner in which foreclosure proceedings take place. State law will determine the method of foreclosure which must be used. Generally, the rules when using a Deed of Trust allow for a faster foreclosure time than with a judicial foreclosure required with a mortgage. Under a Deed of Trust, when the borrower defaults on the loan, the lender delivers the Deed of Trust to the trustee, who then is instructed to sell the property.

After proper notices have been posted and rules are followed, the property is sold at a trustee’s sale and the loan is paid. Be careful not to confuse a deed, which conveys title and is evidence of ownership to property, with a Deed of Trust, which is a means of securing a note and providing for foreclosure proceedings.

Note that Nationatar’s 12/1/14 claim that it had acquired Bank of America’s interest in the Hansen deed of trust was fraudulent and Nationstar rescinded it on 3/8/19. Nationstar did not have a recorded claim to the Hansen deed of trust until one week after discovery ended, and that 3/8/19 claim was fraudulent as well.

According to Nationstar’s attorneys, Nona Tobin is NOT entitled to due process before her property was confiscated by Nationstar whose claims were all fraudulent.

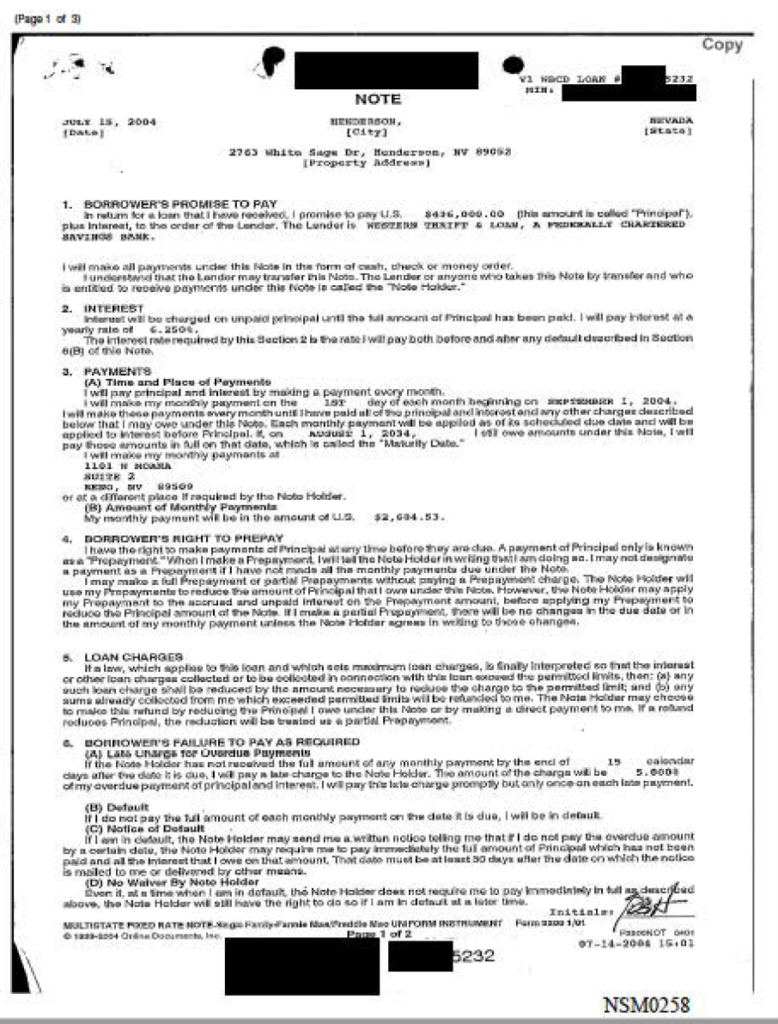

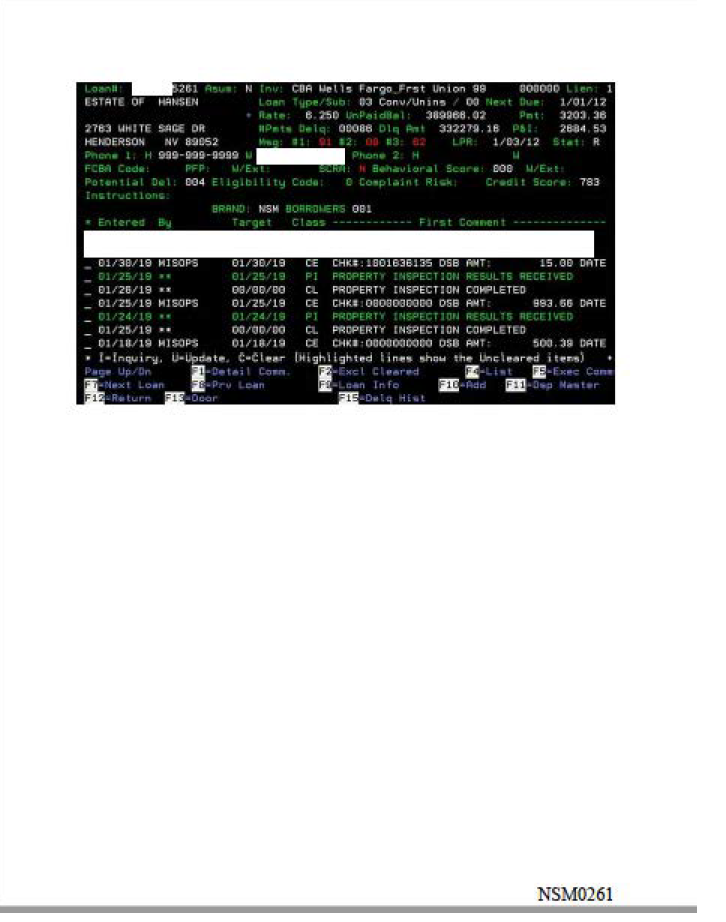

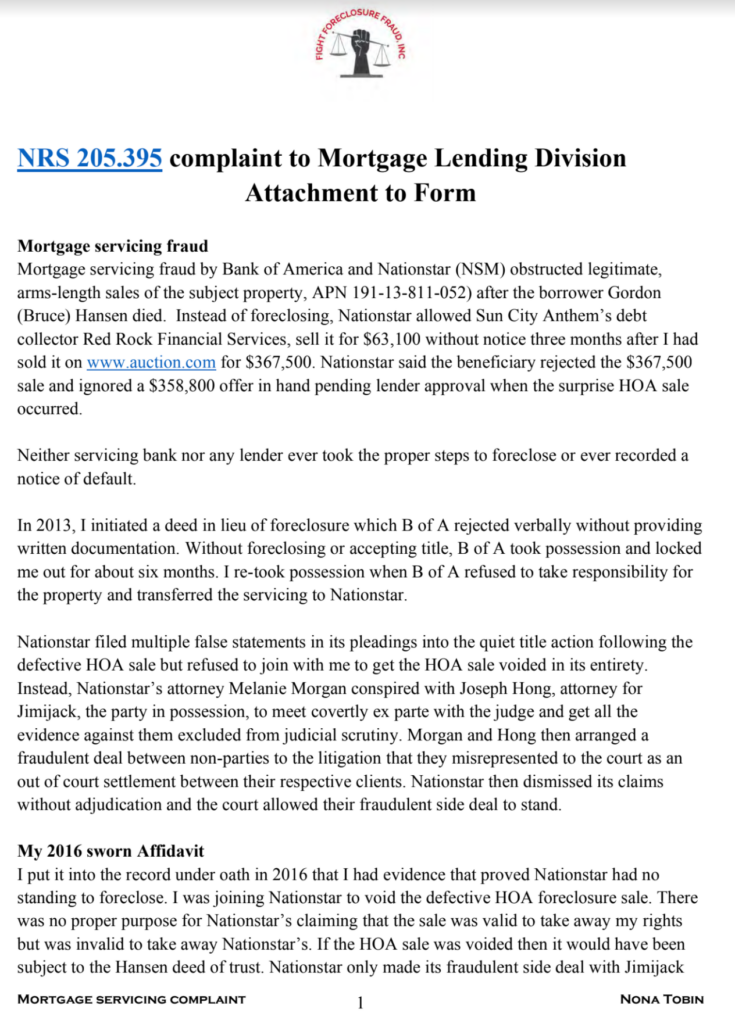

The dispute is over a $436,000 Western Thrift & Loan Deed of Trust (DOT) executed by Gordon Hansen on 7/15/04. Nationstar serviced the loan beginning on 12/1/13 on behalf of an investor NSM refused to identify.

On 12/1/14, Nationstar recorded a claim that Nationstar was owed the $389,000 balance that remained outstanding after the borrowerʼs death.

(b) Representations to the Court. By presenting to the court a pleading, written motion, or other paper — whether by signing, filing, submitting, or later advocating it — an attorney or unrepresented party certifies that to the best of the person’s knowledge, information, and belief, formed after an inquiry reasonable under the circumstances:

(1) it is not being presented for any improper purpose, such as to harass, cause unnecessary delay, or needlessly increase the cost of litigation;

(2) the claims, defenses, and other legal contentions are warranted by existing law or by a nonfrivolous argument for extending, modifying, or reversing existing law or for establishing new law;

(3) the factual contentions have evidentiary support or, if specifically so identified, will likely have evidentiary support after a reasonable opportunity for further investigation or discovery; and

(4) the denials of factual contentions are warranted on the evidence or, if specifically so identified, are reasonably based on belief or a lack of information.

No bank foreclosure was ever initiated on the Hansen deed of trust. Nationstar just stole it.

Neither servicing bank, (Nationstar succeeded Bank of America as servicing on 12/1/13) foreclosed on the Hansen DOT even though it was in default after Hansen died on 1/14/12.

Had Nationstar been the beneficiary of the DOT, it would have foreclosed or collected the debt by allowing the property to be sold at fair market value. NSM did not record a notice of default on the Hansen DOT.

Nationstar did not allow the property to be sold to MZK for $367,500 on 5/8/14. Nationstar did not complain when RRFS rejected its 5/28/14 super-priority offer of $1100 to close the MZK escrow.

Nationstar allowed the property to be sold for $63,100 while a $358,800 was pending lender approval .

Then, three months after the HOA foreclosed to collect $2,000 in delinquent HOA dues, NSM claimed that Bank of America gave NSM the Hansen DOT on 10/23/14.

Nationstar recorded and filed false claims and dismissed all its claims without adjudication

Nationstar prevailed despite ALL declarations under penalty of perjury support Nona Tobin and not Nationstar, by tricking the court into ignoring all the evidence, such as…

No affidavits support Nationstar’s claims, but so what?

In its 3/27/17 OMSJ, Nationstar claimed that on 12/1/14 Wells Fargo had given NSM the DOT. This was supported by a duplicitous declaration regarding business records.

Link to 3/8/19 Nationstar rescission of its 12/1/14 claim that Bank of America assigned its interest to Nationstar

In February 2019, Nationstar refused to produce any documents in response to Tobinʼs RFDs and interrogatories to prove any of its claims.

On 3/8/19, Nationstar recorded that it rescinded its 12/1/14 claim that it got its interest from Bank of America, and then two hours later recorded that it had Wells Fargoʼs undisclosed power of attorney to give Nationstar the authority to assign Wells Fargoʼs non-existent interest to Nationstar.

Nationstar produced no proof that it owned the Hansen DOT during two lawsuits over the validity of the HOA sale.

All the evidence Nationstar entered into the record actually proved the opposite, but it was never subjected to judicial scrutiny Nationstar.

The real owner of the Hansen DOT would have supported Tobinʼs efforts to void the sale so the DOT would not have survived as it the sale had never happened.

Tobin and Nationstar were initially aligned to get the court to void the HOA sale until Nationstar learned that it would be impossible to foreclose on Tobin since Tobin had put it into the record that she had documents that could prove NATIONSTAR did not have the standing to foreclose.

Nationstarʼs covert deal with Joel Stokes was solely to prevent the Court from conducting an evidentiary hearing that would have exposed the inconvenient truth that neither Nationstar nor Stokes could prove their claims.

Nationstar was excused from trial by saying all claims had been resolved by Nationstar-Jimiack settlement.

The HOA wrongly foreclosed, but not without Nationstarʼs assistance.

The banks could have stopped the HOA from foreclosing by recording a Notice of Default (NRS 116.31162(6)).

The HOA sale should have been cancelled when BANAʼs agent tendered $825 on 5/9/13 to cure the nine months that were then delinquent.

The HOA sale would have been avoided if the serving banks had not prevented four escrows from closing as escrows instructions were to pay the HOA whatever it demanded.

The HOA sale would have been avoided if Nationstar had not rejected the 5/8/14 $367,500 www.auction.com sale to MZK Properties.

Nationstar, the servicing bank that is supposed to be a fiduciary, acting on behalf of the investor, turned a blind eye to an 8/15/14 HOA sale for 18% of the $367,500 www.auction.com sale price that Nationstar had just rejected.

NATIONSTAR does not hold the original Hansen promissory note.

NSM 258-259 is a COPY of the Hansen promissory note that Nationstar entered into the record to trick the Court.

NSM does not have Hansenʼs original note, but NSM tried to conceal that fact by disclosing a COPY in NSM 258

NRS 52.235 “Original required. To prove the content of a writing, recording or photograph, the original writing, recording or photograph is required, except as otherwise provided in this title.”

NSM 260 shows no endorsement of Hansenʼs note to Nationstar or to ANY of the lenderʼs NSM claims assigned the note to Nationstar.

3/27/17 NSM filed a DECL that misrepresents its servicing bank record to deceive the court that NSM had no proof it owned the DOT

All Nationstar’s and Bank of America’s recorded actions affecting the Hansen deed of trust are fraudulent

All Nationstar’s disclosures in discovery were deceptive and fraudulent

Wells Fargo did not assign anything to Nationstar.

Page 7 is Morgan’s totally deceptive ploy to obfuscate the fact that Nationstar has no valid claim to be the beneficiary.

Servicing banks (those that handle the paperwork on behalf of the “beneficiary” who is the investor to whom the debt is actually owed).

The dispute with Nationstar is not because Nationstar wrongly foreclosed on the Hansen deed of trust.

The dispute is caused by:

Both BANA & Nationstar obstructing multiple fair market value, arms-length sales, approved by the Hansen Estate.

Nationstar’s letting the HOA foreclose without notice for 18% of the $367,500 www.auction.com sale that Nationstar had just rejected, and then

After the Hansen DOT was extinguished by the HOA foreclosure, Nationstar lied on the record about being owed the $389,000 outstanding balance on Hansenʼs DOT.

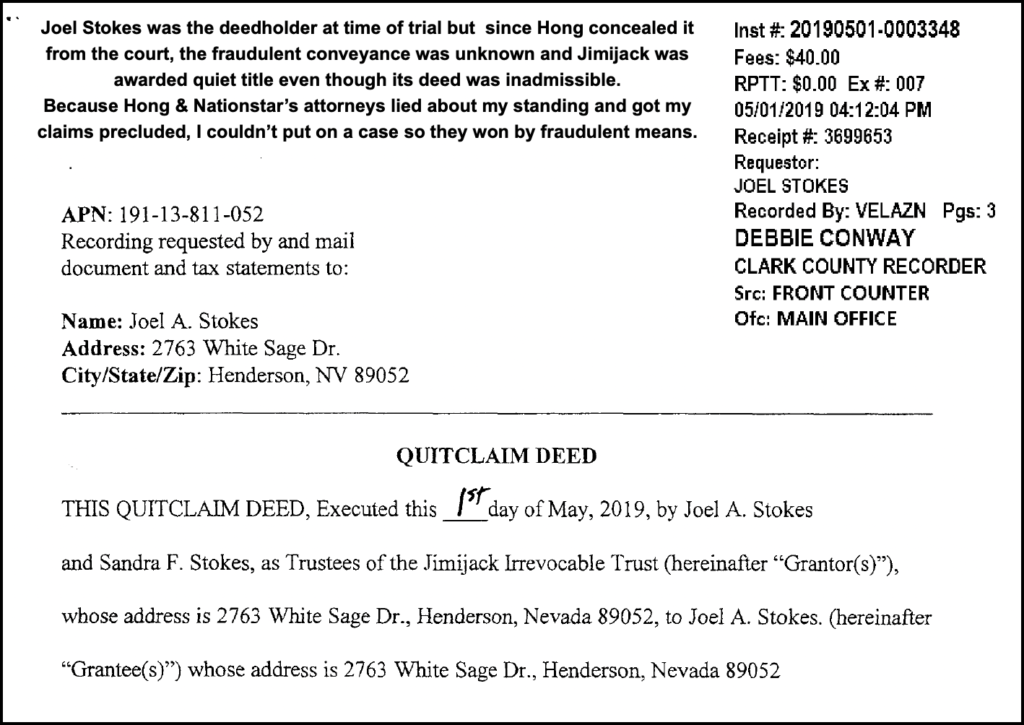

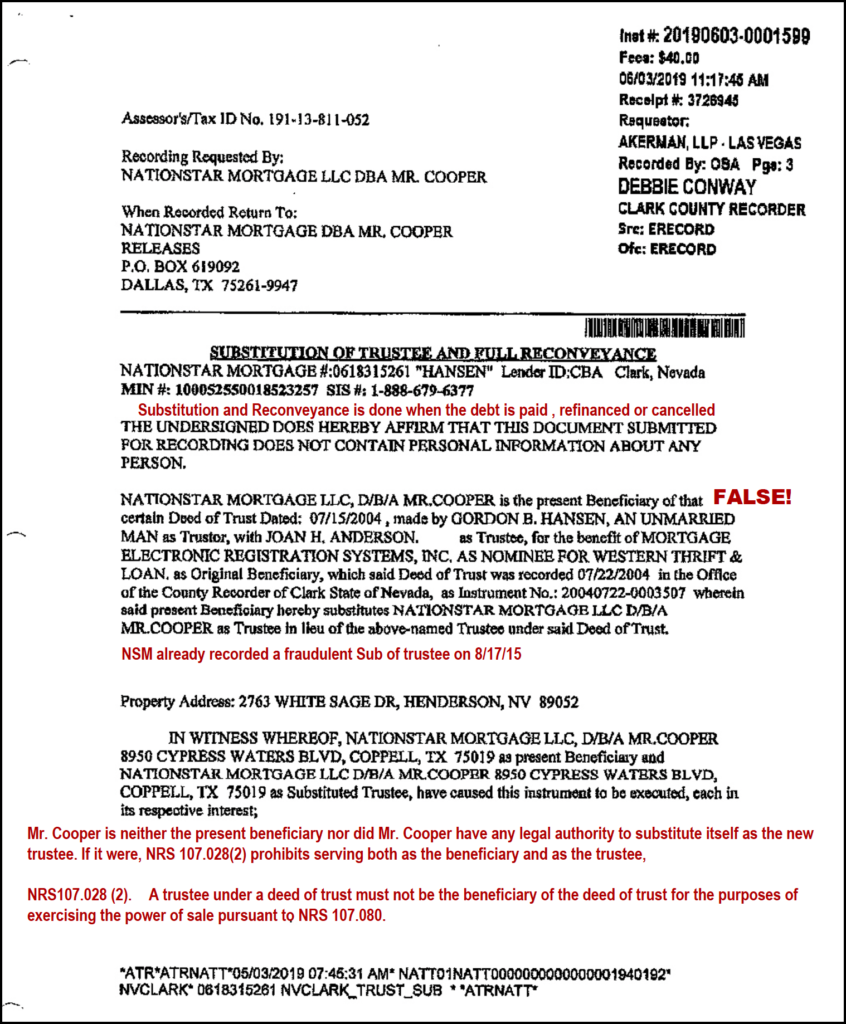

According to NRS 107.28, (2.) A trustee under a deed of trust must not be the beneficiary of the deed of trust for the purposes of exercising the power of sale pursuant to NRS 107.080, but Nationstar claimed to be both the beneficiary and the trustee – when it was neither – and reconveyed the property to Joel Stokes on 6/3/19 to steal the house from Nona Tobin

The Clark County Recorderʼs Office Property Record shows NSM began recording conflicting claims on 12/1/14, more than three months after the HOA sale.

Nationstar lied in its 1/11/16 complaint to say that some unspecified entity had assigned its interest to Nationstar on 2/4/11

BANA & NSM recorded 11 claims regarding the Hansen DOT, but neither ever recorded a Notice of Default, the mandatory condition precedent to the trusteeʼs executing the power of sale on behalf of the beneficiary.

No bank has the right to confiscate a property without foreclosing by following the notice and due process steps defined in NRS 107.080, as amneded by AB 284 (21011), Nevada’s anti-foreclosure fraud law.

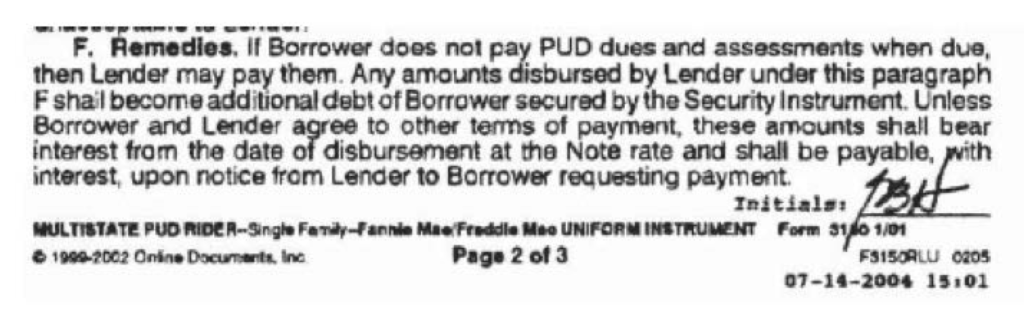

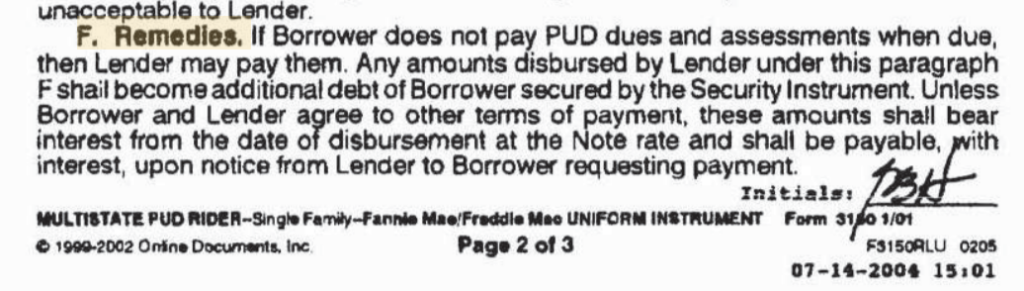

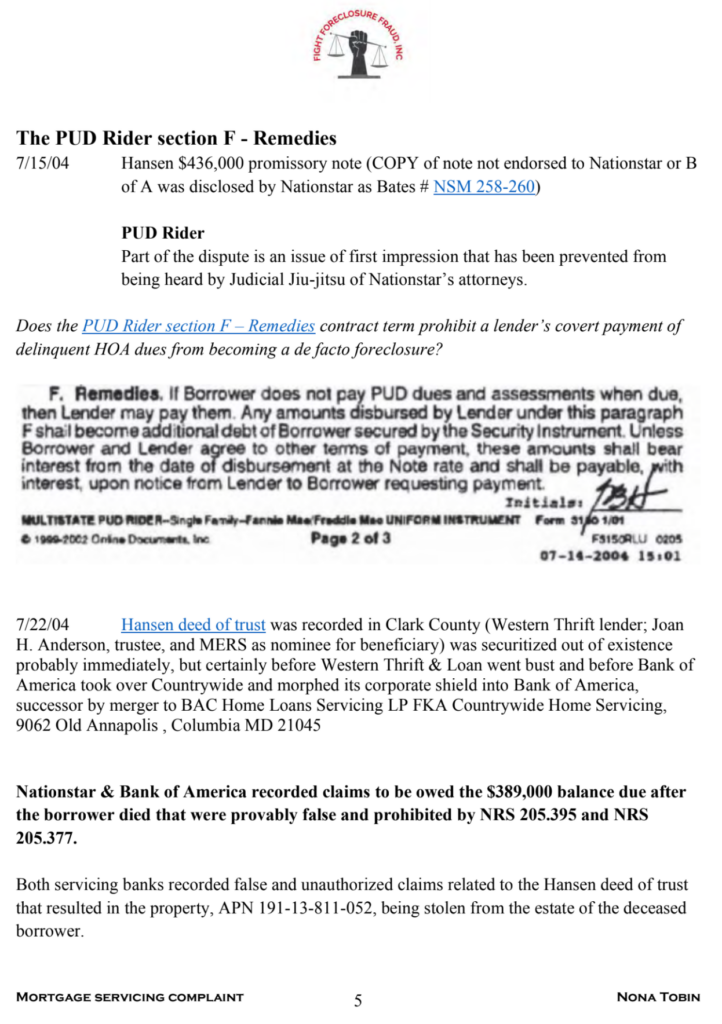

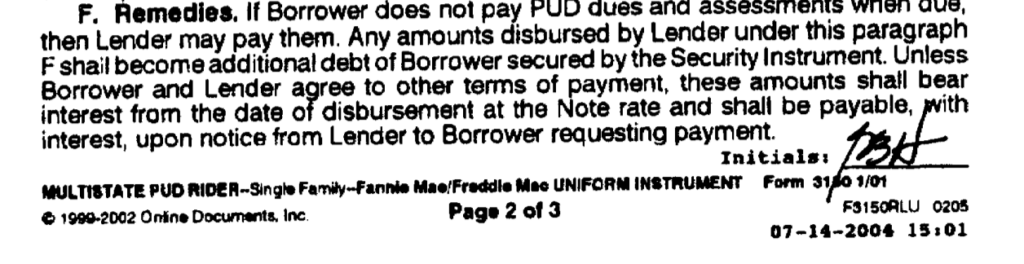

The P.U.D. RIDER must be enforced to protect HOA homeowners from corporate corruption.

The banks deceived the Courts about the “F. Remedies” contract term in the Planned Unit Development Rider.

This scheme isn’t just how Nationstar stole a house from me.

This is the same ploy that many, many banks have used to steal many, many houses from HOA homeowners.

It works because the HOA debt collectors conspired with the corrupt attorneys/lenders to conceal the existence of the PUUD Rider Remedies from the owners and from the courts.

Nationstar knew the PUD Rider remedy limits, but misrepresented it.

Nationstar disclosed the Hansen deed OF TRUST as NSM 141-162.

The Planned Unit Development Rider Remedies F was disclosed as NSM 160. In the 2004 Recorded documents, it is numbered 2004 021 RECORDED.

it is the featured image of this blog and it is pictured again below.

If a lender pays late HOA dues, the ONLY recovery is the amount paid with interest charged at the note rate.

PUD rider remedies f. provides that lenders are contractually authorized only to add delinquent HOA assessments to the outstanding loan balance and add interest at the note rate (here 6.25%).

Lenders are prohibited from using the tender, offer or payment of delinquent assessments, rejected or not, as a de facto foreclosure to confiscate an owner’s property without due process.

Nationstar disclosed the PUD Rider Remedies section so ignorance cannot be an excuse when Nationstar filed its duplicitous 2/12/19 joinder in order to get rid of the owner without foreclosing.

Nationstar was not ever owed Hansen’s debt

Nationstar disclosed that it does not hold the origInal note by disclosing a copy as NSM 158-160.

NSM’s copy of the note shows Nationstar, Wells Fargo and bank of Amercia are not in the chain of title of endorsements.

Criminal penalties must be applied.

All recorded assignments of the Hansen DEED OF TRUST that culminated in Nationstar reconveying the Hansen DEED OF TRUST to Joel Stokes, an individual, on 6/3/19, were false claims to title in the meaning of NRS 205.395.

Evidence in this case has been submitted to administrative enforcement agencies